Whiskey Product Portfolio Optimization Case Study

When I first looked at the brand's overall performance over the past two years, what caught my attention was the complaints around the 18YO product and a 19% revenue decline despite significant marketing spend. My initial instinct was that 12YO was pulling demand away from 18YO, creating a false read on where the real problem was. Part of why I thought that: I had already looked at competitor data and most of them were leaning premium. That made me think the market itself was moving in that direction. But the further I got into the customer data, the clearer it became the problem wasn't 12YO. The problem was 18YO itself and how it was being positioned. Customers weren't turning it down because it was expensive. They just couldn't see why it was worth more than the 12YO sitting right next to it on the shelf. That realization shifted the entire direction of my analysis. And the competitive data was actually pointing the same way: there was a real, unfilled gap in the everyday-use segment exactly where 12YO sat. So instead of recommending a repositioning push for 18YO, I made the case for simplifying the portfolio. I reallocated €1.52M in marketing budget and projected a €125K revenue uplift in Year 1 without increasing total spend.

Business Context

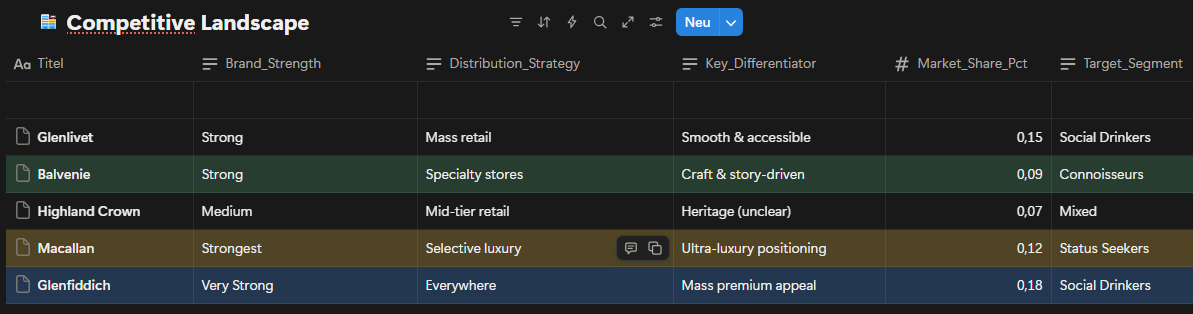

This is a case study I built for my portfolio, based on a hypothetical premium whisky brand. The dataset was constructed using AI, designed to reflect realistic market dynamics drawn from publicly available industry benchmarks. The brand operates in the premium single malt whisky market a space where competing on price alone doesn't get you far. Heritage, storytelling, and how clearly a product earns its place on the shelf matter just as much as the price tag. And there will always be customers willing to pay in this category. That's exactly why sales here depend so heavily on perception, not just on the product itself. The portfolio runs across three age expressions: 12YO (€65), 18YO (€145) and 21YO (€320) each theoretically targeting a different type of buyer. Looking at the competitive landscape, the picture is clear: Glenfiddich owns mass-premium, Macallan anchors ultra-luxury, Glenlivet holds accessible premium. Each of them knows exactly what it is. And that clarity is precisely what makes the problem sitting between 12YO and 18YO so visible and so urgent.

What the competitive map makes clear is that the gap between mass- premium and ultra-luxury isn't just about price it's about perception. Brands that hold that space successfully don't compete on cost. They compete on narrative. Trying to write a new narrative for 18YO would have been, frankly, a bit of a wishful move. But 12YO keeps the door open. Particularly through sustained B2B partnerships bars, cocktail venues, on-trade channels 12YO has a real shot at becoming the lead player in this portfolio.

This analysis highlights a clear gap between mass-premium and ultra- luxury positioning, where differentiation relies less on price and more on perceived expertise, storytelling, and channel strategy.

The Problem Statement

Despite significant marketing investment (€1.52M in 2024), the portfolio began to show structural weaknesses that negatively impacted both revenue and brand perception:

12YO dominance created internal cannibalization:

With 660 units sold annually and the highest value- for-money perception, 12YO increasingly attracted customers who would otherwise consider 18YO, weakening the mid-tier product’s role.

18YO suffered from unclear positioning:

Positioned between volume-driven 12YO and prestige- driven 21YO, 18YO lacked a distinct identity, resulting in a 19% year-over-year revenue decline and growing customer perception that it was “not worth the premium over 12YO.”

21YO faced pressure to justify its premium price:

While maintaining strong brand prestige, declining volumes (-11% YoY) indicated rising expectations from status-driven buyers and increased sensitivity to perceived value versus ultra-luxury competitors.

The competitive landscape highlights that brand naturally attracts connoisseurs and flavor-driven customers through its craft and story-driven positioning. This creates an opportunity to target customers seeking depth and authenticity rather than mass accessibility. At the same time, competitors such as Glenfiddich benefit from aggressive marketing and broad distribution, allowing them to stabilize or even grow sales despite market pressure. Competing directly on mass retail or aggressive marketing would move our brand away from its core audience. For status-oriented buyers, clear ultra-premium signaling is required, as they tend to anchor their perception around strong, easily recognizable luxury cues.

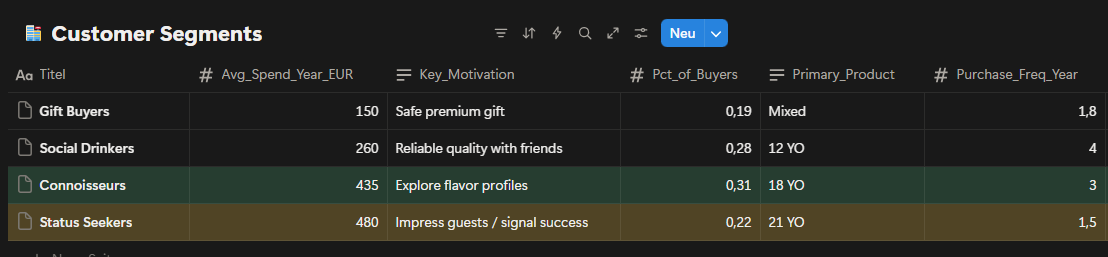

Customer segmentation reveals four clearly defined groups with distinct motivations and spending behavior. Connoisseurs show strong interest in 18YO, while Status Seekers gravitate toward 21YO and demonstrate the highest average annual spend. Powever, the data also indicates overlap between segments, particularly around premium expectations. While Connoisseurs value flavor exploration, their hesitation to commit to 18YO makes it difficult to fully convert interest into consistent purchases. Additionally, overall spending data suggests that Status Seekers spend more per location, which reduces the effectiveness of broad, location-based programs and increases the importance of precise product positioning.

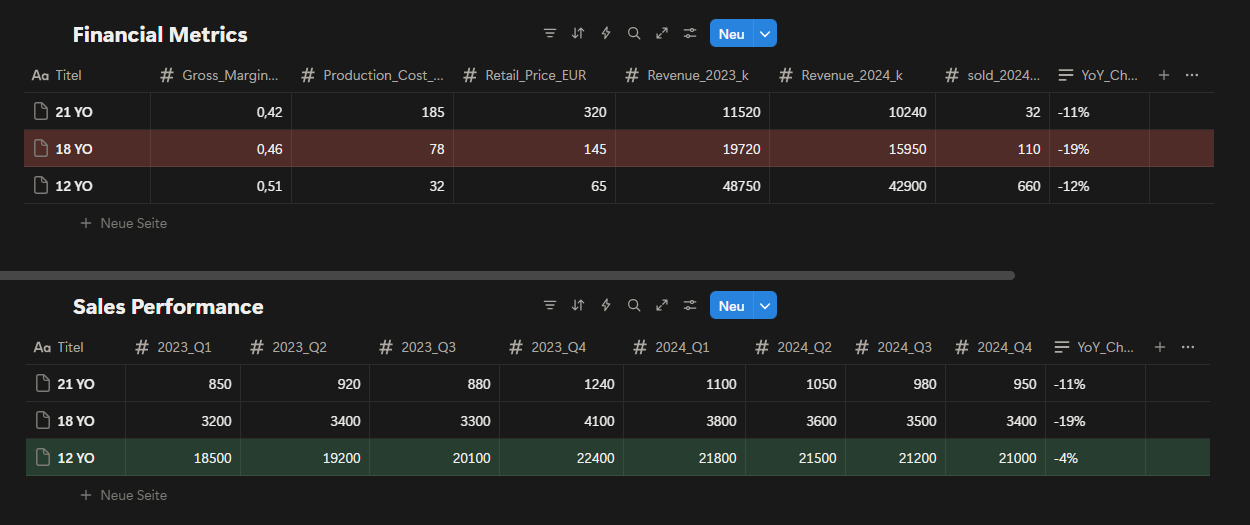

Financial and sales performance data confirms that 18YO has experienced the sharpest decline across the portfolio. Despite relatively healthy margins, both revenue and unit sales have dropped significantly, indicating weakening willingness to pay rather than cost inefficiency. In contrast, 12YO remains highly resilient due to its strong value-for- money perception, while 21YO’s decline reflects rising expectations within a very specific and demanding customer group. This pattern supports the conclusion that 18YO’s challenges are primarily psychological and positional, rather than operational or market driven.

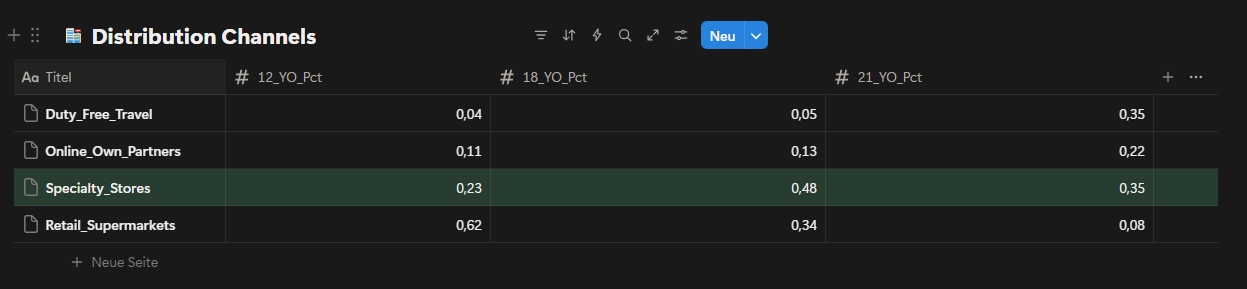

The distribution data shows that specialty stores play a disproportionately important role for 18YO and 21YO compared to mass retail channels. While retail supermarkets dominate 12YO sales, their impact on higher-age expressions is significantly lower. Given this structure, allocating additional resources to mass retail channels would not materially support premium objectives. Specialty stores are already aligned with the intended target audience and should remain the primary focus for premium portfolio execution. Other channels, such as duty-free and online partners, remain secondary and are currently too distant from the desired outcome to justify increased investment.

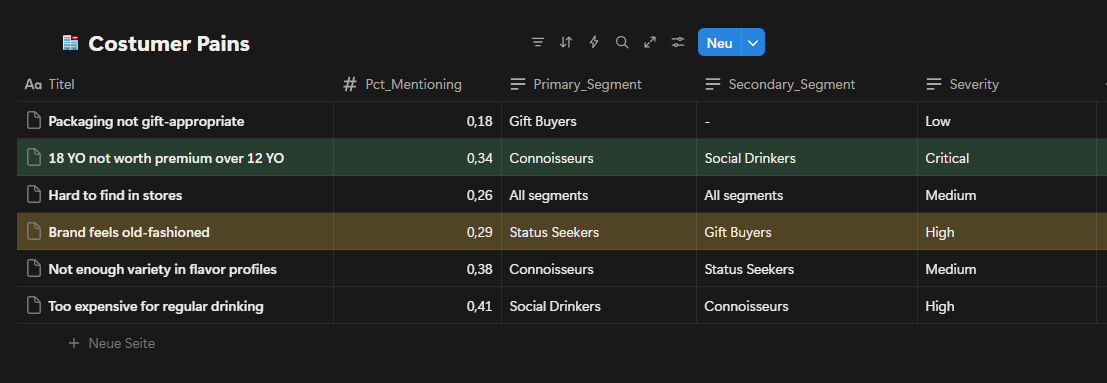

Customer pain points clearly indicate that the most critical issue centers around 18YO’s perceived value. The complaint “18YO not worth premium over 12YO” appears with high frequency and critical severity, particularly among Connoisseurs. This confirms that the challenge is not lack of interest, but a mismatch between price, expectations and communicated value. Additional concerns around brand perception and flavor variety further reinforce the need for clearer differentiation rather than increased promotional activity. These insights suggest that without addressing value perception, further investment in 18YO marketing would deliver diminishing returns.

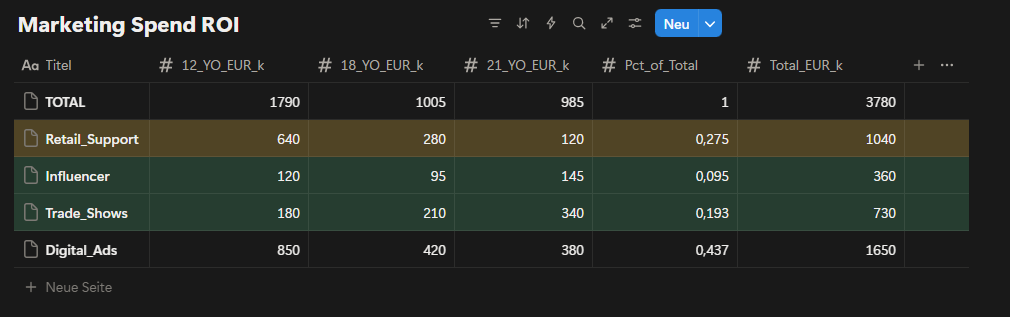

Marketing spend analysis shows that a significant portion of investment is allocated to channels that primarily support 12YO volume rather than premium value creation. By discontinuing 18YO-focused campaigns, a substantial budget becomes available for reallocation. Redirecting part of this budget toward strengthening brand perception and premium signaling creates an opportunity to reinforce both 12YO and 21YO without increasing total spend. In particular, reallocating funds from generic digital advertising toward more targeted channels improves alignment with premium objectives. Overall, this creates approximately €1.52M in available marketing capacity that can be used more strategically.

Proposed Marketing Reallocation

With 18YO marketing discontinued, approximately €1.52M becomes available for reallocation. Rather than increasing total spend, this budget will be redistributed to better support our simplified two-product portfolio.

Current Allocation (2024):

Digital Ads: €1,650K (43.7%)

- Broad reach campaigns targeting volume.

- Primarily attracts Social Drinkers (lower margin segment.

- ROI: ~2.5:1.

Retail Support: €1040K (27.5%)

- Generic POS materials and promotions.

- Not tailored to premium positioning.

- ROI: ~2.2:1.

Trade Shows: €730K (19.3%)

- Industry events and whisky festivals.

- Good access to Connoisseurs and Status Seekers.

- ROI: ~3.8:1.

Influencer: €360K (9.5%)

- Limited partnerships, underutilized channel.

- Strong fit for brand storytelling.

- ROI: ~3.2:1.

Proposed Allocation (2025):

Digital Ads: €400K (-40%)

- Shift from volume to premium targeting.

- Focus on Connoisseurs and Status Seekers.

- Better creative emphasizing craft and heritage.

Retail Support: €500K (-52%)

- Focus only on specialty stores, not mass retail.

- Premium display materials for 12YO and 21YO.

- Co-funded partnership program.

Trade Shows: €500K (+71%)

- Increase presence at high-end whisky events.

- VIP experiences for 21YO buyers.

- Direct access to status-driven customers.

Influencer: €420K (+192%)

- Expand to 15–20 premium lifestyle and whisky content creators.

- Long-form storytelling about craft and quality.

- Builds brand aura supporting both 12YO and 21YO.

TOTAL: €1,520K (neutral budget)

This reallocation moves spending away from channels that support volume and toward channels that support premium perception and brand strength. Trade Shows and Influencer channels show the highest ROI and best alignment with our target segments, which is why they receive the largest increases. The shift happens gradually over six months to allow time for new partnerships to develop and campaign creative to be produced.

Product attribute scores reveal a clear imbalance in perceived value. While 18YO performs well on complexity and smoothness, its value-for-money score is significantly lower than both 12YO and the competitor average. This gap explains recurring customer dissatisfaction and reinforces price resistance. Without visual, experiential, or narrative upgrades, 18YO will continue to trigger friction at the point of purchase. Conversely, improving brand aura and visual perception around 12YO offers an opportunity to elevate perceived value without changing price.

Across all datasets, the evidence consistently points to a portfolio design issue rather than a demand shortage. The core challenge lies in how value is communicated and perceived across age expressions, with 18YO positioned in a way that creates friction instead of progression.

Strategic Options:

Option 1: Aggressive Premium Repositioning of 18YO

Strategy:

Reposition 18YO as a clearly premium product by increasing its price and limiting availability, aiming to close the perceived gap with 21YO.

Key Actions:

- Increase 18YO retail price to reinforce premium perception.

- Restrict distribution primarily to specialty stores.

- Shift messaging toward exclusivity and craftsmanship.

- Reduce mass-market visibility to avoid comparison with 12YO.

Expected Outcome:

This approach could improve perceived value and margins if accepted by Connoisseurs, but carries a high risk of volume loss due to existins price sensitivity and weak value-for-money perception.

Risks:

- Strong resistance from customers already questioning 18YO value.

- High probability of accelerated sales decline.

- Increased internal competition with 21YO.

Option 2: Portfolio Clarification by Phasing Out 18YO (Preferred)

Strategy:

Remove 18YO from the active portfolio and simplify the value ladder by focusing on a clear two-step progression: 12YO for quality-driven volume and 21YO for status-driven premium demand.

Key Actions:

- Discontinue 18YO-focused marketing activities.

- Redirect freed marketing budget toward brand strengthening initiatives.

- Enhance visual identity and perceived value of 12YO.

- Reinforce ultra-premium signaling for 21YO through selective channels.

Expected Outcome:

By eliminating internal cannibalization and psychological friction, the portfolio becomes easier to understand. This strengthens trade-up logic toward 21YO while preserving 12YO’s strong volume base.

Why This Option:

- Directly addresses the most critical customer pain point.

- Frees approximately €1.52M in marketing capacity without increasing spend.

- Aligns with observed customer behavior and spending patterns.

- Reduces complexity and execution risk.

Risk Analysis

While Option 2 offers the clearest path forward, it carries meaningful risks that require active management. Removing 18YO eliminates €15,950 in annual revenue. Not all of this revenue will automatically transfer to other products.

Downside Scenario:

If customer behavior does not follow expectations, the following outcomes are possible:

- 50% of current 18YO buyers move down to 12YO (55 customers)

Revenue gain: 55 × €65 = €3,575 - 20% trade up to 21YO (22 customers)

Revenue gain: 22 × €320 = €7,040 - 30% leave for competitors such as Glenfiddich or Macallan (33 customers)

Revenue lost: 33 × €145 = €4,785

Net Impact:-€5,335 (-8% of total portfolio revenue)

This scenario becomes more likely if customers are not actively guided through the transition. To reduce this risk, a 90-day customer retention program will start in Month 1, including direct outreach to former 18YO buyers and targeted incentives to encourage trial of 21YO. Removing 18YO creates a gap in the €145–200 price range, which competitors may see as an opportunity.

Likely Scenarios:

Scenario 1:

Glenfiddich reduces the price of their 18YO from €175 to €135. Position 12YO as better value ("Why pay €135 for 18 years when you can get quality at €65?") and accelerate brand elevation work to strengthen 12YO perception.

Scenario 2:

Macallan launches a new mid-tier product priced around €160. Double down on 21YO exclusivity and heritage positioning, where Macallan cannot fully match our craft story. Competitor pricing and product launches will be monitored monthly during the first six months, with flexibility to adjust strategy if market conditions change significantly.

Retailer Relationship Risk

Specialty retailers currently generate revenue from three Balvenie products. Reducing the portfolio to two SKUs may reduce shelf presence and total sales for these partners.

Retailer Concern:

"If Balvenie reduces my revenue, why should I give you premium shelf space?"

To address this, a three-part specialty store partnership program will launch in Month 1:

- Margin improvement — Increase 21YO retailer margin from 25% to 30%.

Cost: €512 per year, securing long-term relationships. - Co-funded displays — €2,000 per store for premium in-store setups.

Total investment: €40K across 20 key locations. - Staff training & events — Product education sessions and customer tasting events.

Total investment: €65K.

This approach keeps retailers engaged and motivated to promote the remaining portfolio despite a reduced SKU count.

Customer Confusion Risk:

Some customers who actively searched for 18YO may feel confused or frustrated when it is no longer available.

To manage the transition smoothly, the following steps will be taken:

- Month 1 — Inform specialty retailers first and provide clear talking points for staff.

- Month 2 — Email past 18YO buyers with a personal explanation and a one-time 15% discount on 21YO.

- Month 3–6 — Monitor customer service inquiries and retailer feedback on a weekly basis.

If confusion or negative sentiment exceeds 20% of feedback, additional communication materials will be created or a limited farewell edition will be considered to ease the transition. These risks are real but manageable. Success depends on staying close to the data during the first six months and responding quickly if customer behavior deviates from projections.

Recomendation

Based on the analysis, I recommend phasing out 18YO from active portfolio focus and simplifying the value ladder around two clearly differentiated products: 12YO as the quality-driven volume anchor and 21YO as the status-driven premium expression. This approach directly addresses the root causes identified in customer pains, financial performance, and marketing efficiency, while minimizing execution risk and preserving long-term brand equity.

This recommendation was selected because it:

- Eliminates internal cannibalization between 12YO and 18YO.

- Removes the most critical customer pain point around value perception.

- Frees marketing capacity without increasing total spend.

- Strengthens portfolio clarity and trade-up logic.

- Aligns with observed customer behavior rather than forcing repositioning.

Implementation will follow a phased and controlled approach:

Phase 1: Portfolio Reset (Months 1–2)

18YO-related marketing activities are discontinued. Existing inventory is managed through natural sell-through without promotional pressure.

Phase 2: Brand Reinforcement (Months 3–6)

Freed marketing budget is redirected toward strengthening brand aura and visual perception, with a focus on modernizing 12YO communication and reinforcing premium cues around 21YO.

Phase 3: Premium Focus Optimization (Months 6–12)

Selective channels such as specialty stores, trade shows, and targeted digital placements are used to support 21YO visibility and reinforce status- driven demand.

Success will be evaluated using the following metrics:

- Stabilization of total portfolio revenue year-over-year.

- Reduction in customer complaints related to value perception.

- Improved marketing efficiency measured by ROI per channel.

- Increased share of premium sales driven by 21YO.

- Clearer product understanding reported by specialty retailers.

Primary Metrics (Business Impact):

Total portfolio revenue: Maintain ≥ €69M per year.